Introduction

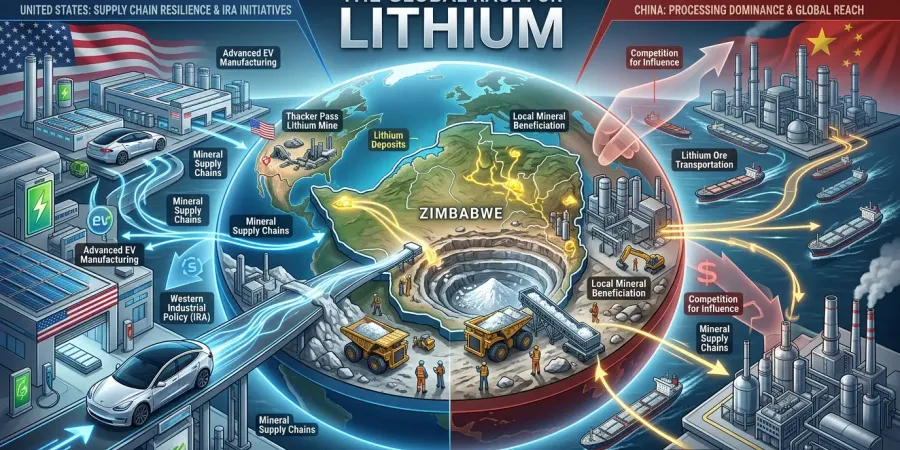

The global transition toward electric vehicles (EVs), renewable energy systems, and advanced battery storage technologies has intensified geopolitical competition over access to critical minerals. Lithium has become strategically important because it is essential for lithium-ion batteries used in EVs, renewable energy storage, and emerging technologies tied to artificial intelligence and defense industries. As demand rises, the U.S. and China are increasingly competing to secure reliable lithium supply chains.

Zimbabwe has emerged as one of Africa’s most significant lithium producers due to its large, untapped reserves and increasing foreign investment activity. Simultaneously, the U.S. has accelerated efforts to reduce dependence on Chinese-controlled mineral supply chains through domestic industrial policies such as the 2022 Inflation Reduction Act (IRA) and strategic projects such as Thacker Pass Lithium Mine. However, U.S. domestic production alone is unlikely to satisfy future lithium demand, making overseas sources such as Zimbabwe strategically important.

This report analyzes how U.S.-China geopolitical competition is shaping investment opportunities and operational risks within Zimbabwe’s lithium sector, particularly for major EV manufacturers, including Tesla, BYD, Volkswagen, and General Motors, and multinational investors seeking exposure to African critical mineral markets.

Zimbabwe’s Strategic Lithium Landscape

Zimbabwe possesses extensive mineral wealth, including gold, platinum, chrome, nickel, and lithium deposits. Lithium has become the centerpiece of recent investment activity because of soaring global demand for EV battery materials. Zimbabwe is believed to hold some of Africa’s largest hard-rock lithium reserves, positioning the country as a growing supplier within the global energy transition.

Several major projects demonstrate the strategic importance of Zimbabwe’s lithium industry. In 2021, Chinese company Zhejiang Huayou Cobalt acquired the Arcadia Lithium Mine near Harare for approximately $422 million. Arcadia is expected to become one of Africa’s largest lithium operations and a major supplier for China’s battery industry. Similarly, Chinese-owned Sinomine Resource Group acquired Bikita Minerals in 2022, further expanding China’s influence over Zimbabwe’s lithium sector.

China’s investment strategy reflects a vertically integrated supply-chain model. Chinese firms are not only acquiring mines but also investing in infrastructure, mineral processing, and refining capabilities. China already dominates global lithium refining capacity, meaning that even lithium mined outside China often remains dependent on Chinese-controlled processing infrastructure.

Recognizing lithium’s strategic value, Zimbabwe implemented a ban on the export of raw lithium ore in December 2022. The policy was designed to force mining firms to process lithium domestically instead of exporting unprocessed ore abroad. Zimbabwe hopes the policy will increase industrialization, employment, and foreign currency earnings through local beneficiation and value addition.

However, the export ban also creates new challenges for investors. Mining firms may now need to build domestic processing facilities, increasing capital requirements and exposure to infrastructure shortages, energy instability, and regulatory uncertainty. While the policy creates opportunities for long-term industrial investment, it also raises operational risk for multinational corporations.

Thacker Pass and the Limits of U.S. Domestic Supply

The development of Thacker Pass in Nevada, U.S. demonstrates why Zimbabwe remains strategically important despite U.S. efforts to increase domestic lithium production. Operated by Lithium Americas Corp., Thacker Pass is one of the largest known lithium deposits in the U.S. and has become central to American critical mineral policy.

The project aligns closely with the IRA, which incentivizes EV manufacturers to source battery minerals from the U.S. or allied partners in order to qualify for federal tax credits. Tesla has signed agreements connected to Thacker Pass as part of its effort to secure IRA-compliant battery supply chains and reduce dependence on Chinese processing networks.

Despite strong political support, including a reported $2.3 billion government-backed loan commitment, Thacker Pass illustrates the limitations of relying solely on domestic production. The project has faced years of environmental litigation, permitting disputes, and Indigenous land-rights concerns. These delays demonstrate how difficult and time-consuming large-scale mining development can be in the U.S.

Even if Thacker Pass reaches full production capacity, projected U.S. lithium demand is expected to exceed domestic output for years due to EV expansion, battery manufacturing growth, and rising energy-storage requirements. As a result, companies such as Tesla will continue seeking diversified foreign lithium supplies.

Zimbabwe therefore becomes strategically important not as a replacement for U.S. domestic mining but as part of a broader diversification strategy. Thacker Pass reinforces the need for geographically diversified supply chains across North America, Latin America, Australia, and Africa.

U.S.-China Geopolitical Competition

Competition over Zimbabwe’s lithium sector reflects a broader geopolitical struggle between the U.S. and China for control over future energy and technology supply chains. China currently maintains a significant advantage due to its early investments in African mining assets and downstream processing infrastructure.

The U.S. increasingly views critical minerals as a national security issue. Under the IRA, EV tax credits require increasing percentages of battery minerals to come from the U.S. or allied countries rather than “Foreign Entities of Concern,” including China. The policy is intended to reduce dependence on Chinese-controlled supply chains while encouraging investment in alternative sourcing partnerships.

However, Western firms face difficulties competing with China’s investment model in Zimbabwe. Chinese companies often benefit from state-backed financing, infrastructure agreements, and long-term diplomatic relationships that enable rapid project development. By contrast, many Western corporations remain cautious due to governance concerns, sanctions-related uncertainty, and ESG considerations.

Zimbabwe’s relationship with the West has also been shaped by longstanding political tensions and targeted U.S. sanctions on specific individuals associated with corruption and governance concerns. Although these sanctions do not broadly prohibit mining investment, they contribute to investor caution and reduce Western corporate engagement.

As geopolitical tensions increase, African mineral-producing states such as Zimbabwe are becoming central arenas for strategic competition. Control over lithium supply chains increasingly influences industrial policy, energy security, and technological competitiveness.

Investment Opportunities and Risks

Zimbabwe offers substantial investment opportunities because of its large lithium reserves and growing importance within the EV economy. Companies capable of navigating regulatory complexity may gain access to increasingly valuable mineral supplies.

For Tesla, diversified lithium sourcing is essential for maintaining long-term battery production growth. Zimbabwe’s lithium sector could provide supply-chain benefits through partnerships with processors, refiners, or non-Chinese operators capable of meeting Western sourcing standards.

However, operational risks remain significant. Zimbabwe continues to face political instability, currency volatility, corruption concerns, and infrastructure deficiencies. Electricity shortages, transportation bottlenecks, and limited industrial processing capacity increase operational costs for mining firms.

The lithium export ban itself creates uncertainty because investors may fear additional regulatory interventions or shifting ownership requirements. Geopolitical tensions between the U.S. and China may further complicate supply chains if trade restrictions intensify.

ESG concerns also present reputational risks. Investors increasingly face scrutiny regarding labor practices, environmental management, and community relations in extractive industries. Companies perceived as contributing to exploitative resource extraction may face regulatory and reputational consequences in Western markets.

Recommendations

Multinational corporations and investors should adopt a diversified and risk-conscious approach toward Zimbabwe’s lithium sector.

First, firms should avoid overdependence on any single supplier or country. Tesla and other EV manufacturers should combine domestic projects such as Thacker Pass with overseas sourcing from Africa and allied states.

Second, investors should prioritize partnerships that support local processing and infrastructure development within Zimbabwe. Firms aligned with Zimbabwe’s beneficiation goals may receive more favorable long-term political treatment.

Third, corporations should conduct rigorous political risk assessments and closely monitor evolving regulations surrounding export controls, sanctions exposure, and ownership requirements.

Finally, multinational firms should strengthen ESG compliance and community engagement programs to reduce reputational risk and improve operational stability.

Conclusion

Zimbabwe’s lithium industry demonstrates how critical minerals have become central to geopolitical competition between the U.S. and China. While China currently dominates much of Zimbabwe’s lithium sector, the U.S. increasingly seeks diversified mineral sourcing to reduce supply-chain vulnerabilities and strengthen industrial resilience.

The development of Thacker Pass highlights both the importance and limitations of domestic U.S. lithium production. Despite growing American investment in domestic mining, overseas sources such as Zimbabwe will remain strategically important because of rapidly increasing global demand.

Zimbabwe’s lithium export ban reflects the country’s attempt to capture greater economic value from its mineral wealth, but it also introduces new operational challenges for multinational investors. Companies capable of balancing geopolitical awareness, regulatory adaptation, ESG compliance, and supply-chain diversification may gain significant advantages within the rapidly evolving global battery economy.